Winning examples from first direct, Aviva and NS&I GPS

Customers have varied banking products and often these are held with many different providers. Understanding these products and tracking where money is being spent or saved is very difficult when there is not one single platform to help. Some consumers also want other options to expand their finances, increase their credit history (even if they are renting their property) or check if there are more relevant offers available.

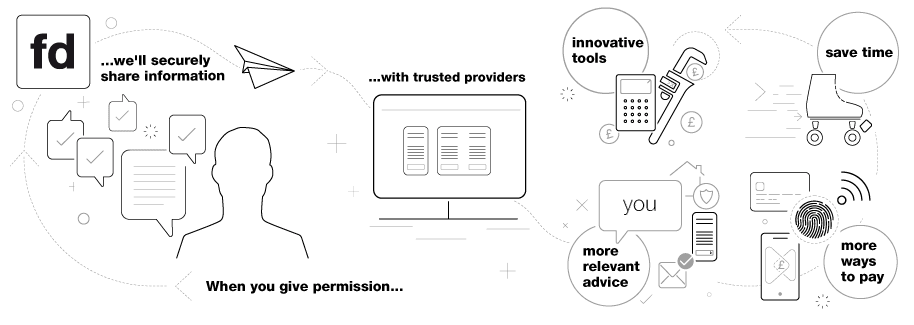

What was the solution? first direct wanted to solve all three of these problems for customers in a way that similar competitor solutions had been unable to. It would push the boundaries of what is possible using both aggregation and acquisition tools. The app had to be one simple, easy to use platform which would allow customers to categorise specific transactions and personalise their experience.

artha by first direct embraced the new world of Open Banking by delivering Marketplace Banking, the first major UK bank to make third party financial and non-financial products available to customers within a banking app. The app combined regulated financial products including investments, unsecured loans, and credit cards, as well as non-financial products and services such as utility switching. Some of the third-party providers in the marketplace include American Express, Nutmeg, Wealthify, MoneyFarm, and Flipper.

The project team also wanted to solve the problem that first-time buyers often face – renting their houses while not gaining any credit score benefit by doing that. Using the government scheme “Rental Recognition”, artha sought to be the only financial management app to allow its users to register for this scheme.

How was it implemented? They decided a fintech company would be able to move at pace and push out new innovations at a faster rate than they could themselves. Together, through the FCA Sandbox, first direct and Bud developed a standalone app and made it accessible via the Apple App Store to both first direct and non-customers. During the 6-month trial at the start of 2018, there were 6,000 users with 1,000 non-first direct accounts connected. This allowed them to test new innovations and changes in a controlled environment to see how they were accepted.

After the Sandbox conclusion, they conducted many test and learn activities with both users and non-users alike to really understand what the appropriate markets were looking for.

The results Through the FCA trial, customers utilised the service to open financial products not currently offered by first direct which has generated revenue from third party affiliate fees. A good example is Flipper, an energy switching company, which converted 6 leads from 39 interested parties - a rate of 15.38% (the highest conversion rate).

Qualitative feedback found 74% of users that connected accounts found aggregating their financial information either quite useful or very useful.

Retention rates are considerably higher than other finance apps with an average of 86% of customers logging in per month. 58% found their spending categorised either quite or very useful, and 21.5% utilised ‘lists’ of which 55% found it either quite or very useful. This was above anticipated and highlights the demand for custom categorisation per user.

Quote Manipulation is a major fraud risk in retail motor insurance, which previously went undetected.

Across Aviva they have a shared passion to help make claims simpler, easier and effortless for customers. That meant finding a way to quickly identify those who manipulate key facts to obtain policies or premiums they are not entitled to, while protecting genuine, honest customers looking for a simple and fair premium.

Doing so would help keep premiums down and improve the claims experience.

What was the solution? Aviva needed an automated Real-Time solution that was fully integrated with workflow tools to identify fraud at the point of quote instead of at the point of claim. They needed to find a way to cross reference quote behaviour against known fraud data and tools, creating a predictive model to identify quote manipulation. Real-Time capability would remove complexity and friction from the process and prevent people fraudulently misrepresenting risks when accessing Aviva products.

How was it implemented? Working in an agile way and deploying systems thinking principles, this was a collaborative ground-breaking product delivery across Fraud, Analytics & IT. Together, they found a way to: • Identify customers deliberately manipulating material facts during the quote process. • Identify customers who were able to “cloak” their fraudulent behaviour by modelling quotes to get an outcome that they wanted, before proceeding to purchase (or present themselves “clean” to another brand or channel). • Use data modelling to identify anomalous and fraudulent patterns in Motor quote activity and create a set of business rules for scoring and referring quote applications in the moment. • Access and match against multiple identifiers on circa 300 million Aviva live quotes across all Direct and Indirect Channels. • Enable multiple fraud decisions depending on severity which could be updated in real time.

The results A fully automated solution at point of quote is now used across Aviva’s UK business, Quote Me Happy, GA and intermediated channels.

• No impact on a genuine customer’s purchase journey, and a quote decision that takes just 0.3 seconds. • Claims teams can focus on settling claims from genuine customers. • Premiums for genuine customers are lower. • The customer experience is continually improved as they learn more about customer behaviour from a significant new data asset. • They have seen a 25% incremental uplift in fraud detection. • Average of 3 million quotes screened per day, delivering savings in excess of £7 million. • Deterred potential fraudsters = a significant financial benefit.

Empowering working people on low incomes to build their savings and encourage an ongoing savings habit is not easy. But that’s the challenge the Government set NS&I Government Payment Services (NS&I GPS), in collaboration with HM Revenue & Customs (HMRC), HM Treasury (HMT) and the Department for Work and Pensions (DWP).

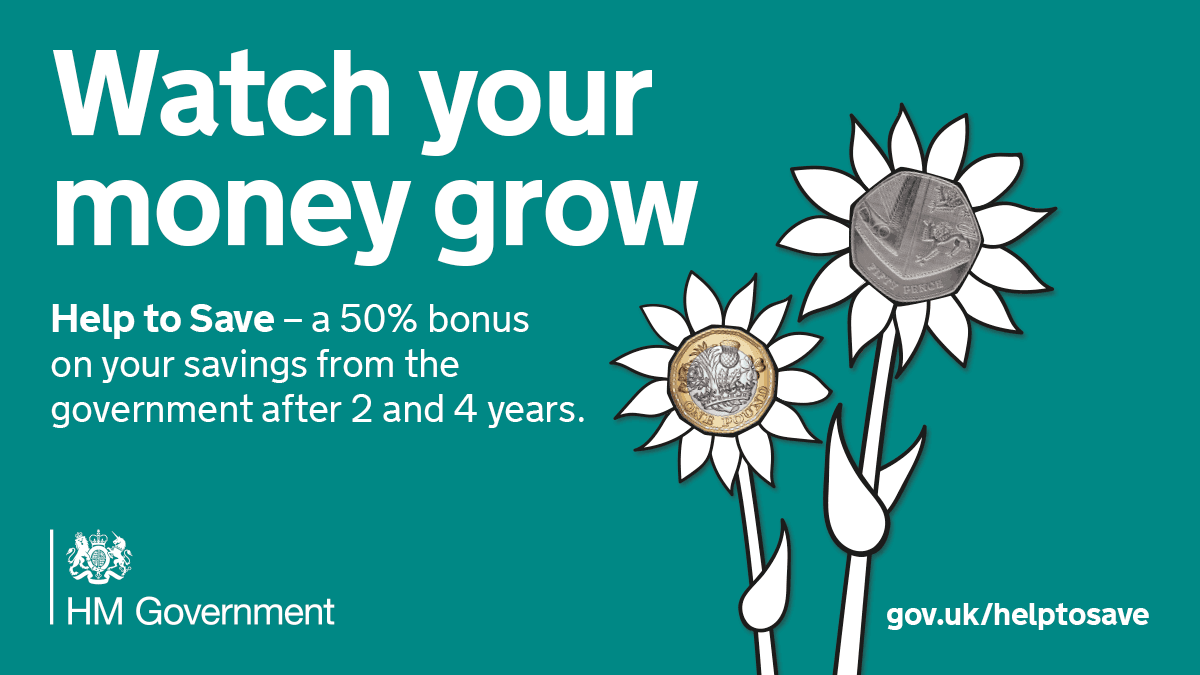

What was the solution? The Help to Save scheme was set up to develop a ‘digital first’, easy, safe and secure way for an eligible population of approximately 3.5 million people receiving Working Tax Credit or Universal Credit to start saving and receive additional government support. Eligible applicants can save between £1 and £50 a month in their Help to Save account and get a bonus of up to 50p for every £1 put in, up to a maximum of £600 over two years. Savers can then continue to use Help to Save for a further two years and earn up to another £600 i.e. save up to £2,400 and get bonuses worth up to £1,200 (tax-free). Withdrawals can be made without penalty.

How was it implemented? The team adopted a highly collaborative approach between NS&I GPS, HMRC, HMT and DWP, underpinned by clear, robust governance. The programme worked transparently, flexibly and seamlessly across all four organisations and multiple suppliers to embed a successful ‘test and learn’ approach.

The solution had to: • Integrate new and existing IT systems and operations across NS&I GPS, HMRC, DWP and HMT so that real-time customer eligibility checks were possible, and accounts were created by NS&I GPS. • Create a seamless customer journey that delivered the objective of helping people on low incomes to develop a savings habit. • Deliver high levels of customer satisfaction, putting the digital service first, while providing offline support to those who need it. • Integrate with HMRC’s Personal Tax Account app so that customers can check their account balance and transactions on the app with their smart phone. The result is more regular checking of their account which supports the policy objective of encouraging a savings habit.

The results The public launch was a success and the Help to Save programme was held up as ‘an exemplar’ in an Office of Government Commerce (OGC) Readiness for Service Review. Strong cross-departmental leadership and close cooperation reduced costs and ensured the private pilot phase was delivered to scope in January 2018. In 2019, the Help to Save programme passed all three Government Digital Service (GDS) Assessments first time and met all 18 standards.

By the end of July 2019, more than 132,000 people had opened accounts with Help to Save and deposited over £31 million. The service has won four awards for Financial Inclusion, Investments, Customer Service; and System and Service Interoperability.